Optimize your b2b cash flow now. Contact Bridge Capital Partners for expert ach payment processing solutions. Call us today or visit our blog for more insights.

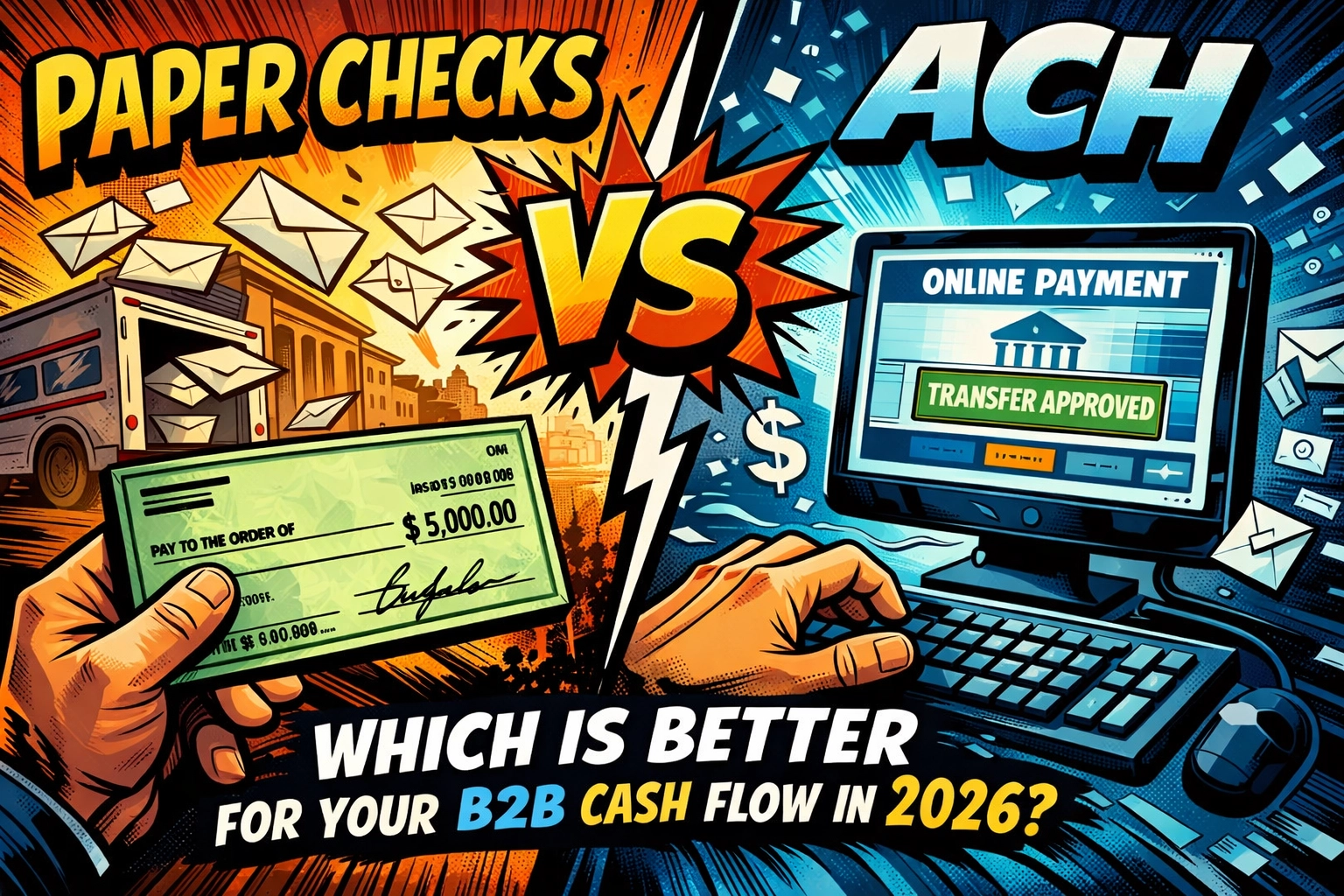

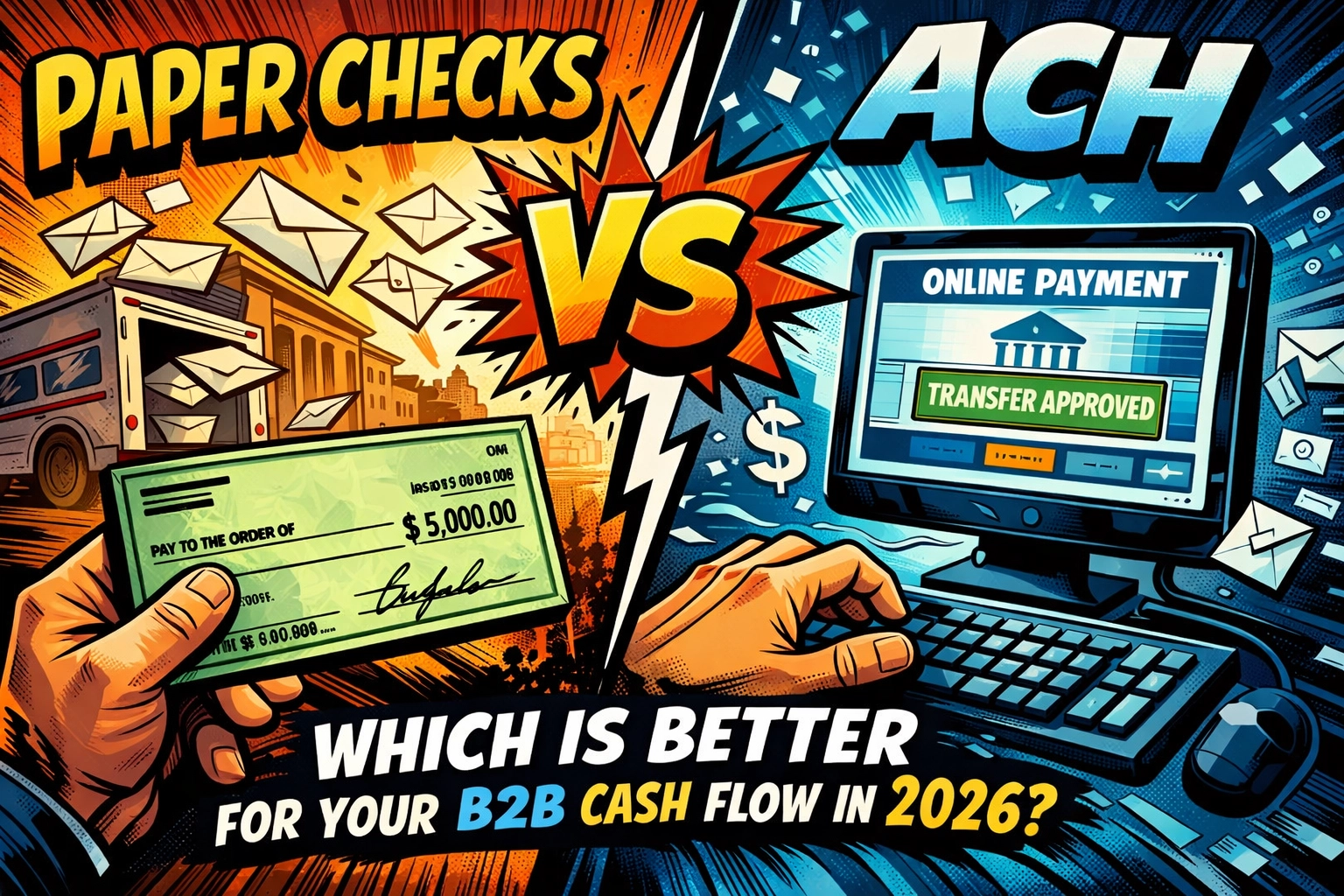

The 2026 Reality Check: Is Your Payment Strategy Stuck in 1996?

It is March 2026. If you are still opening envelopes, squinting at messy handwriting, and driving to a physical bank to deposit rectangular slips of paper, we need to have a serious talk. Your competitors are likely running circles around you using automated systems, while you’re stuck playing "Where’s Waldo?" with your accounts receivable.

Paper checks were great when gas was $1.20 and the internet came on a CD-ROM. But in today’s economy, they are the anchor dragging down your b2b cash flow. Enter ACH (Automated Clearing House). It isn’t just a "digital check": it’s a high-speed lane for your capital.

If you want to stop chasing payments and start scaling, you need to understand the fundamental shift happening in the financial landscape this year.

The Cost of Convenience: By the Numbers

Let’s talk about money. Specifically, how much of yours is disappearing into the void.

Processing a paper check isn't just about the stamp. It’s the labor of the person opening the mail, the data entry, the risk of "the check is in the mail" lies, and the bank fees for manual processing. Industry data for 2026 shows that the average cost to process a paper check can reach up to $20 when you factor in administrative time.

In contrast, ach payment processing costs a fraction of that. We’re talking anywhere from $0.20 to $1.50 per transaction.

Visual: A comic book style panel showing a "Business Hero" battling a giant, sentient paper check monster that is eating money bags.

Think about your margins. If you’re processing 100 B2B payments a month, moving to ACH could save you thousands in overhead. That’s capital you can reinvest into growth, marketing, or finally getting that espresso machine for the breakroom. For a deeper dive into how pricing structures work, check out transparent credit card processing pricing secrets.

Speed and the "Float" Myth

There used to be a strategic reason to use checks: the "float." You’d send a check on Friday, knowing it wouldn't hit your account until Wednesday. You were essentially borrowing time.

In 2026, the float is dead. Banks have gotten faster, and Nacha (the folks who run the ACH network) has implemented Same-Day ACH as a standard. While a check might still clear in a day or two once deposited, the delivery time is the killer.

ACH is predictable. You know exactly when the money leaves your account and exactly when it hits your vendor’s account. This predictability is the secret sauce for healthy b2b cash flow. When you can forecast your balance with 99% accuracy, you can make bolder business moves. If you're wondering how this compares to newer tech, read our breakdown on ACH vs Real-Time Payments.

Security: Why Checks Are a Fraud Magnet

If you wanted to design a payment method specifically to help criminals, you’d design the paper check. It has your account number, your routing number, and your signature right there on the front. It’s a "how-to" guide for identity theft.

Check fraud has skyrocketed over the last two years. Mail-box fishing and "check washing" (where thieves use chemicals to erase the payee and amount) are at all-time highs.

ACH, however, is encrypted and transmitted through secure bank channels. It’s reversible in cases of error, but it cannot be "forged" in the traditional sense. By moving to ach payment processing, you are effectively locking your vault door. For businesses in high-risk sectors, this security isn't just a perk: it's a survival requirement. If you’re in a "tricky" industry, you might also want to look at securing your high-risk merchant account.

Visual: A comic book panel featuring a high-tech security shield deflecting "Fraud Bolts" away from a digital ACH symbol.

Compliance: Staying on the Right Side of Nacha

In 2026, Nacha isn't playing games. They’ve updated rules regarding data validation and fraud detection for ACH users. If you’re handling high volumes of payments: especially in sensitive industries like debt collection: compliance is your shield against massive penalties.

Many businesses stick with checks because they’re afraid of the "tech hurdles" of ACH compliance. This is a mistake. Modern payment gateways handle the heavy lifting for you. Whether you are a small SaaS company or a large-scale agency, mastering compliance is the only way to ensure your b2b cash flow isn't interrupted by a sudden freeze or fine.

For those in the recovery space, we have a specific guide to mastering compliance and cash flow that is essential reading this year.

The Vendor Relationship Factor

"But my vendors like checks!"

Do they? Or do they just like getting paid? Most vendors in 2026 prefer ACH because it means they don't have to send someone to the bank. It means the money is in their account automatically, and the reconciliation is handled by their software.

By offering ACH, you’re becoming a "preferred partner." You’re easy to work with. You’re modern. You’re the company that doesn't make their accounting department pull their hair out. If you’re worried about how to set this up, you should consult with a professional. Learn how to choose the best merchant account broker to find a partner that fits your specific business model.

When (If Ever) Should You Use a Check?

We’ll give checks one thing: they are the ultimate backup. If the power goes out, the internet dies, and the global banking grid takes a nap, a physical check might still get the job done eventually.

Some very small, older contractors might still insist on them. In those rare cases, keep a checkbook in the back of the safe. But for 99% of your B2B transactions in 2026, using a check is like choosing to walk from New York to LA when there’s a direct flight available.

Implementation: How to Make the Switch

Ready to stop the paper chase? Here is your 2026 battle plan:

- Audit Your Payments: Look at how many checks you cut last month. Multiply that by $20. That’s the "Check Tax" you’re paying for being old-school.

- Choose a Processor: Don't just go with your local bank’s basic portal. You want a processor that offers robust reporting and integrates with your accounting software.

- Update Your Contracts: Make ACH your default payment method. Tell your vendors that digital is the new standard.

- Verify Your Data: Use account validation tools to ensure you have the right routing and account numbers. This prevents "failed payment" headaches.

For subscription-based businesses, this transition is even more critical. Check out our guide on choosing ecommerce payment processing for subscriptions to see how recurring ACH can save you a fortune in credit card churn.

Visual: A "Step-by-Step" comic strip showing a business owner transforming their office from a cluttered paper mess to a sleek, digital command center.

Final Verdict

In the battle of Paper Checks vs. ACH, the winner for 2026 is clear. ACH wins on cost, security, speed, and professionalism.

If you want to protect your b2b cash flow, you need to retire the pen and ink. Modernizing your payment stack isn't just an "IT project": it’s a strategic move to ensure your business stays liquid and competitive.

Stop losing money to outdated systems. Reach out to Bridge Capital Partners now for a custom ach payment processing setup. Let’s get your cash flow moving at the speed of 2026.

For more tips on avoiding common pitfalls, see our article on 7 mistakes you're making with your payment processing.

Visual: A final comic panel showing a "Business Champion" standing atop a mountain of successfully processed digital transactions, looking toward a bright horizon.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment